Every two years, the Department of Housing and Urban

Development (HUD) issues its

Worst

Case Housing Needs Report to Congress (WCN). This report highlights the

challenges faced by low-income renter households in finding affordable, good-quality

housing. In addition to data on characteristics of renter households and units,

HUD’s report provides a count of renters facing worst case needs

—defined as households

who earn less than 50 percent of the area median income (AMI) who do not

receive housing assistance from the government, who also are severely cost burdened

(spending more than 50 percent on income on housing costs), and/or live in

severely inadequate units.

In its most recent WCN report released in May 2015,

HUD noted a full 9 percent decline in the number of households with worst case

needs, falling from 8.5 million in 2011 to 7.7 million in 2013. It was the

first decline in that measure since a slight (1 percent) decrease in 2005-2007

and followed two periods of increases of about 20 percent. The change was

surprising given that it coincided with a time of broadly stagnant incomes,

rising rents, and a rapid increase in the number of renters. Do HUD’s numbers

reflect genuine improvements in conditions for renters or are other factors at

work?

A potential explanation for the decrease in worst case needs

explored by HUD is a change in the income limits the agency uses to identify households

earning less than 50 percent of AMI (very low-income households). Between 2011

and 2013, HUD reduced the maximum income for very low-income households by $516,

decreasing the number of households in this group eligible to be counted among

those with worst case needs by about 1 percent. When HUD compared the tallies

of renters with worst case needs using the new and old cutoffs, however, it

found that only 20,000 of the 750,000 total reduction 2011–2013 could be

attributed to the new lower income limit.

Much of the decrease in worst case needs is due to a drop in

households with severe cost burdens, which account for the vast majority of

worse case needs. HUD reported that the total number of renter households with

severe cost burdens fell from 10.4 million in 2011 to 9.7 million in 2013, a

decline of over 6 percent. Counter to these findings, however, calculations

from the Joint Center for Housing Studies (JCHS) using a different data source,

the American Community Survey, found a negligible decline (just over 1 percent)

in severely cost burdened renters, from 11.3 million in

2011

to 11.2 million in

2013.

Notes: Severe burdens are defined as housing costs of more than 50% of household income. In HUD tabulations, households with zero or negative income are excluded unless they pay Fair Market Rent or more for housing. For households paying no cash rent, utility costs are used to represent housing costs. In JCHS tabulations, households with zero or negative income are assumed to have severe burdens, while renters paying no cash rent are assumed to be without burdens.

Sources: HUD Worst Case Housing Needs: 2015 Report to Congress and JCHS tabulations of US Census Bureau, American Community Surveys.

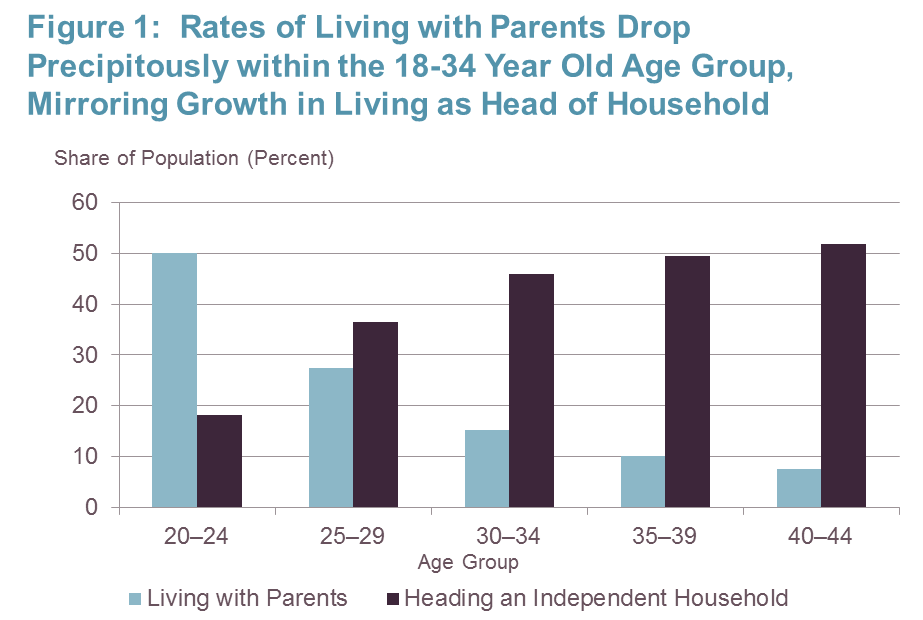

Several unique methodological differences help contextualize

why HUD and JCHS estimates vary

(Figure

1). The first key distinction between the measures reported by HUD and JCHS

is the source data. HUD estimates of cost burdens rely on the

American Housing Survey

(AHS), a biennial survey jointly administered by HUD and the Census Bureau assessing

characteristics of the housing stock and its occupants. JCHS calculates cost

burdens using the

American

Community Survey (ACS), an annual Census Bureau survey of households designed

to supplement the short form decennial census. The surveys vary in size and

scope. The AHS reaches 50,000-70,000 housing units in its national longitudinal

sample, gathering detailed information on housing quality and cost, assisted

status, and location. The ACS reaches 3.0-3.5 million households in the years

since its full implementation and collects information on many demographic,

economic, and employment characteristics, along with selected housing cost and

unit information.

In addition to their variations in design, the AHS and ACS use

distinct methods for defining occupied units that result in different counts

for the most basic variables of total households (equivalent to total occupied

housing units) and households by tenure. While

several

reports

have examined these differences in more depth, essentially the ACS uses a

broader definition of occupancy and makes more attempts to contact sampled

households. These features of the survey tend to increase the number of

occupied units reported and can count households in a seasonal residence (often

rented) rather than their usual residence (possibly owned), increasing the

number of renter households over the AHS

(Figure

2). While not unique to the 2011-2013 period to explain the divergent

trends, this difference in methodology consistently results in about 2 million

more renter households in the ACS over the AHS, likely contributing in part to

a higher ACS count of burdened renters

Sources: HUD Worst Case Housing Needs: 2015 Report to Congress and JCHS tabulations of US Census Bureau, American Community Surveys.

There are also important distinctions in how cost burdens

are measured and what adjustments are made to the data. According to its WCN

report, HUD excludes households reporting zero or negative income when

calculating cost burdens, unless these households report paying the local Fair

Market Rent (FMR) or more for housing. In this case, HUD assumes the negative

income reported to represent a temporary situation and imputes a higher income

for the household. If these households pay more than FMR and live in adequate,

uncrowded housing, an income slightly higher than the local area median is

assigned, again assuming a temporary period of income loss. HUD also makes

adjustments for households that report paying no cash rent. For these

households, HUD relies on reported utility costs to represent housing costs and

identify housing cost burdens.

In contrast, JCHS assumes all households reporting zero or

negative income to be severely cost burdened and all those paying no cash rent

to be unburdened (in the case of a household reporting both zero or negative

income and no cash rent, the household is assumed to be unburdened). The

difference in adjustments may have had an especially large impact in 2011-2013 as

JCHS tabulations of the AHS find the number of renter households reporting zero

or negative income rose by nearly 13 percent, about four times the rate of

growth of renters reporting positive income. ACS numbers do not mirror this

rise, as renters reporting zero or negative income increased by 3 percent

2011-2013. Excluding zero or negative income households may better isolate

households with perennially low incomes from those potentially higher-wealth

households reporting temporary annual business losses. However, excluding these

households from ACS analysis finds that severe cost burdens still do not drop

nearly as much in 2011-2013 as HUD methods shows. Subtracting all households

with zero or negative incomes from the ACS burden count shifts the totals to

10.4 million severely burdened renters in 2011 and 10.3 million in 2013, a

decline of just 1.4 percent—much smaller than that reported by HUD for the

period. Conversely, if all zero or negative income households in the AHS were

considered burdened regardless of rent level, the decline in renters with

severe cost burdens 2011–2013 would be about 4.6 percent.

In addition to varying counts of zero and negative income

households, a disparity in median renter income patterns between 2011 and 2013

may also explain part of the divergent cost burden trends in that period. HUD

cites an increase in median renter income of 7.2 percent in 2011-2013 in real

terms as a factor driving down the number of severely burdened renters. While

JCHS estimates of ACS data also find an increase in real median renter income

in that time—the first increase since 2006-2007—the gain is a distinctly

smaller 5.2 percent. HUD notes in its WCN report that some of the observed

increase in median income may be due to newly formed higher income renter households,

but does not further explore this possibility. Analysis of ACS data indeed

shows that an influx of higher income renters occurred over this time. Of the net

1.7 million increase in renter households measured in the ACS 2011-2013, fully

1 million or 60 percent had incomes of $75,000 or more, over twice the median

renter income (Figure 3). With this

group pulling up the median figure, aggregate income gains may not have

impacted lower income households sufficiently to meaningfully decrease the

number of severely burdened renters.

Source: JCHS tabulations of US Census Bureau, American Community Surveys.

Indeed, analysis of the most recent 2014 ACS reveals the

number of severely burdened renters is once again on the rise, climbing to 11.4

million

—the highest number on record. Whether new AHS data expected in the

upcoming months and the next WCN report due the following spring confirm this

trend or show a further drop in severely burdened renters, the results of both

surveys again underscore the acute unaffordability of housing for millions of

renter households. Understanding whether affordability pressures are worsening

or easing is therefore crucial to making informed decisions concerning rental

assistance and other housing policy actions. Given additional data showing

persistent

rent

growth and

tightness in the rental market, the larger

sample size of the ACS, the benefit of an added year of ACS data showing rising

burdens, and the unusually large recent shifts in renter incomes in the AHS, it

seems likely that the enduringly high severe cost burden levels reported by the

ACS are more accurate and affordability pressures for renter households

continue to build.