|

| by Kermit Baker Director, Remodeling Futures Program |

Why is this likely to occur? To begin, it is worth noting that owners undertaking home improvement projects, even larger projects, rely heavily on savings to pay for these projects. Findings from a October 2016 Piper Jaffray Home Improvement Survey are consistent with previous consumer surveys regarding how owners pay for major home improvement projects. Savings continue to be the principal source of funds as 62 percent of respondents planning a project indicated that they would use savings for all or part of the payment. Another 37 percent said they would put all or part of the cost on a credit card, with many of these planning to immediately pay off their balance. In contrast, only 18 percent said they planned to use a home equity line of credit to fully or partially fund their projects.

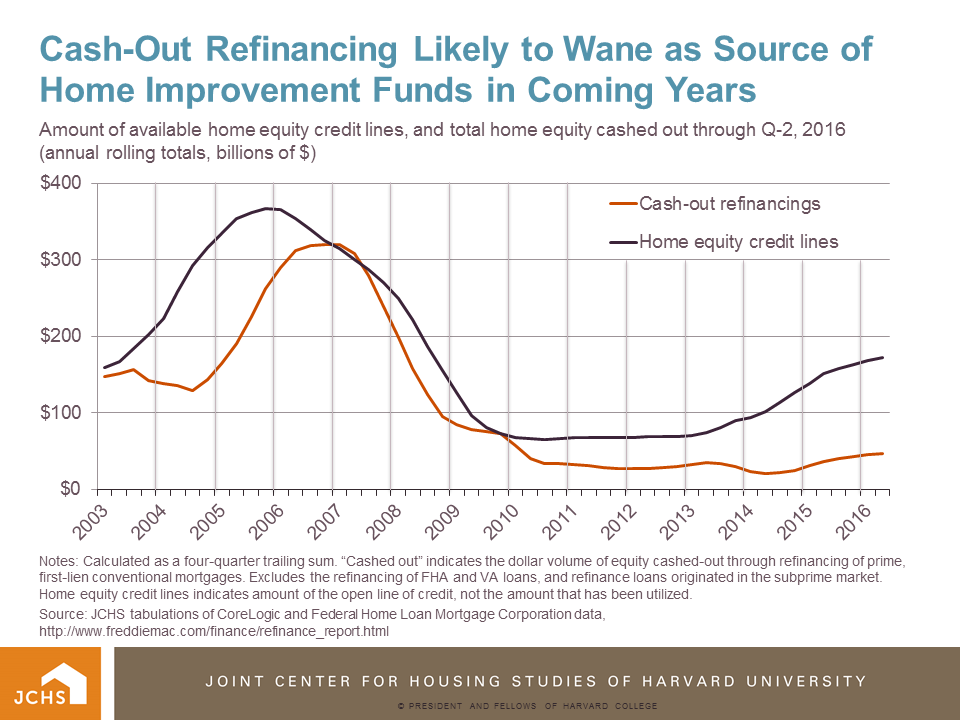

For much of the past decade, the volume of cash-out refinancing has just about equaled borrowing available through home equity credit lines. However, signs are quite clear now that we are at the end of this near decade-long interest rate down cycle. Interest rates on 30-year fixed rate mortgages, which have been trending up since last summer, spiked almost 50 basis points (one-half percentage point) after the presidential election. Noting that the incoming Trump administration is likely to push for tax cuts and infrastructure spending increases, most forecasters are projecting that long-term interest rates will continue to rise in 2017.

While higher interest rates will discourage some owners from cashing out home equity to undertake home improvement projects, they may actually promote remodeling spending by others. How can this be the case? Rising mortgage rates may encourage many owners to remain in their current homes. Interest rates for 30-year fixed rate mortgages have been below 5 percent since early 2011, so virtually everyone who has purchased a home or refinanced their fixed rate mortgage over the last six years has locked into a historically low mortgage rate. This means that if rates rise, trading up to a more desirable home also involves paying off a low interest mortgage and taking out a new higher rate loan. Facing this prospect, many owners may instead decide to improve their current home rather than buying a home with the features they now desire.

Those owners who want to tap into their growing levels of home equity to finance their home improvement projects are likely to rely on home equity lines of credit rather than cash-out refinancing. As long-term rates have stabilized near their cyclical low, we’ve already seen that homeowners are starting to rely more on home equity credit lines. In the coming months as rates trend up, the gap between home equity borrowing and cash-out refinancing is likely to widen, which, unfortunately, will expose these home equity borrowers to future hikes in short-term rates.

Notes: Calculated as a four-quarter trailing sum.“Cashed out” indicates the dollar volume of equity cashed-out through refinancing of prime, first-lien conventional mortgages. Excludes the refinancing of FHA and VA loans, and refinance loans originated in the subprime market. Home equity credit lines indicates amount of the open line of credit, not the amount that has been utilized.

Source: JCHS tabulations of CoreLogic and Federal Home Loan Mortgage Corporation data, http://www.freddiemac.com/finance/refinance_report.html

No comments:

Post a Comment